If you use a credit card, you’ve probably seen the minimum payment due on your monthly statements. While paying only this amount may seem like a good idea, you must understand what managing your finances responsibly means.

What is the credit card minimum payment?

The credit card minimum payment due is the smallest amount you can pay on your credit card balance by the statement due date without incurring late fees and keeping your credit card agreement and your account in good standing.

It’s usually a percentage of your total balance, around 1% to 3%, plus any interest or fees.

Example:

Balance $1,000, minimum payment 2% = $20 plus interest.

Paying only the credit card minimum payment can result in spending more money in interest over a fixed amount of time.

How is the credit card minimum payment calculated?

The calculation of the minimum payment varies by credit card issuer but generally includes:

A percentage of your balance: 1%–3%.

The interest charge added due to the APR.

Late fees or fees over the limit.

What happens if you only make the minimum payment?

If you only make the minimum payment, the remaining balance will accrue interest at the APR.

Over time, this can lead to:

Interest charges add up; you will owe more.

Making only the minimum payment extends the time it takes to pay off the debt.

A high balance to credit limit (utilization) can hurt your credit score.

Your monthly statement should have a 'Minimum Payment Warning' that will tell you how long it will take to pay off your debt.

What happens if you don’t make the minimum payment?

A minimum payment is necessary to avoid late payment fees and a penalty APR.

Missed minimum payments are reported to the credit bureaus and can negatively affect your credit score.

A single missed minimum payment can significantly impact your credit score, as it will be reported to the credit bureaus. This negative mark can take a long time to recover from, making it crucial to always make at least the minimum payment on time.

Paying the minimum credit card payment or missing a payment can result in a late fee.

Some credit cards might increase their annual percentage rate (APR) if a minimum payment is missed.

What is the impact on your credit score?

Consistently making minimum payments can negatively affect your credit scores. Major credit bureaus report late payments, resulting in negative marks on your credit report.

Your credit utilization ratio is an essential factor for calculating your scores.

Paying more than the minimum payment on a credit card saves you money on interest and reduces your credit utilization ratio faster.

Making only the minimum payment on your credit card bill can have a detrimental effect on your credit score and credit utilization ratio. This is a key reason why it's important to pay more than the minimum, as it can help you maintain a healthy credit score.

Payment history makes up 35% of your FICO credit score and 41% of your Vantage Score 4.0 credit score.

What is a reason to pay more than the minimum payment due on your credit card statement each month?

There's not just one but several reasons to pay more than only the minimum payment due.

1. Less interest paid

Credit card interest accrues daily, so the longer you carry a remaining balance, the more interest you pay. Paying more than the minimum amount pays down the principal faster, saving you money in the long run.

2. Pays off debt faster

Paying more allows you to pay off the entire balance much sooner, free up credit, and reduce stress. For example, paying $200 instead of paying the minimum amount of $50 on a $1,000 balance can make a big difference.

3. Credit utilization

Credit utilization—the percentage of your remaining balance to your credit limit—affects your credit score. Paying more than the minimum pays down the balance and lowers your utilization and score.

4. Avoids the debt trap

Making only the minimum payment can lead you into a dangerous debt cycle where balances grow faster than you can pay them off. By paying extra each month, you can break free from this cycle and take control of your debt.

What are some strategies for paying more than the minimum payment?

Here are some strategies I have found that will help you make more than the minimum payment on a credit together.

1. Budget

Set aside a portion of your monthly income to pay down credit card debt.

2. Goal

Pay off a certain percentage of the balance each month.

3. Multiple payments

Pay bi-weekly instead of monthly to pay off the balance faster.

4. Windfalls

Apply bonuses, tax refunds, or unexpected income to your credit card balance.

How can Shoeboxed help manage your minimum payments?

Shoeboxed is an excellent tool for financial organization and expense tracking, so it’s also an excellent tool for paying off credit card debt.

Here’s how Shoeboxed can help you with financial management and avoid the minimum payment trap:

1. Tracks expenses all in one place

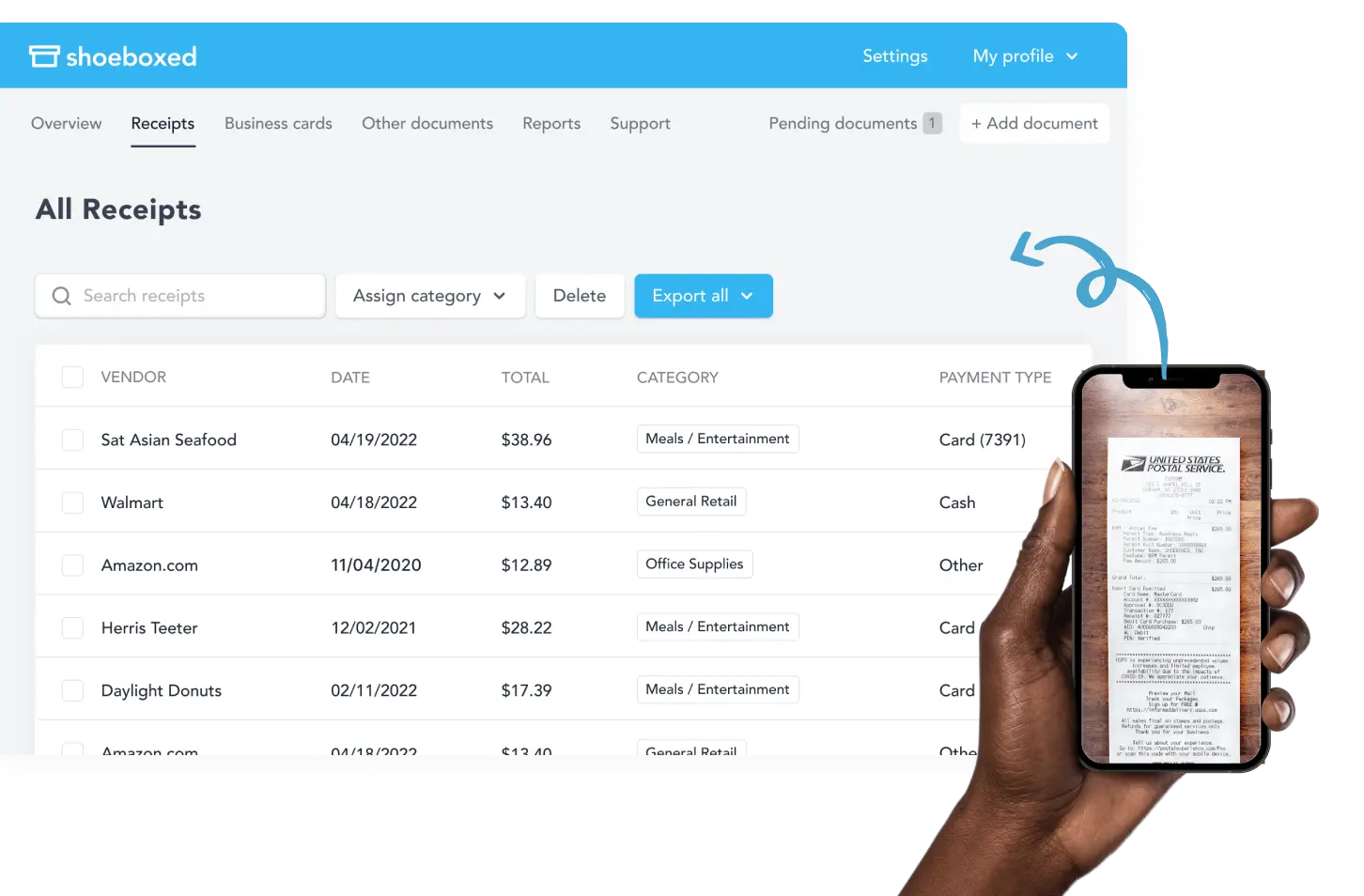

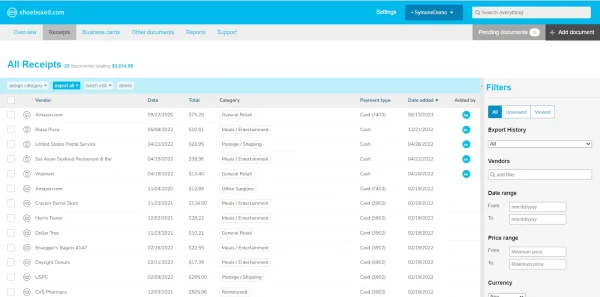

Shoeboxed digitizes your receipts so you can easily keep track of your spending all in one place.

To digitize the transaction, photograph the receipt with your phone's camera. The Shoeboxed app will automatically upload the picture to your designated Shoeboxed account.

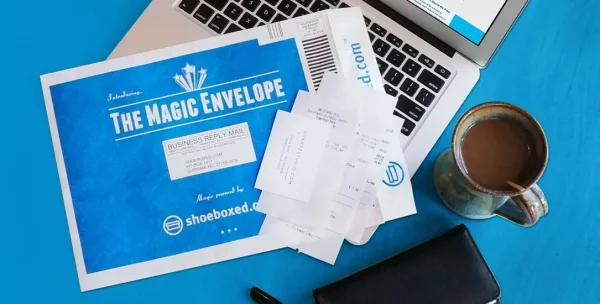

Or, if you have a lot of receipts and don't want to scan them yourself, you can outsource them to Shoeboxed. Mail them via the free postage-paid Magic Envelope service, and they will scan, human-verify, and upload them to your account for you.

That way, you have all your receipts in one place, making them easier to keep up with and track. They're also automated, eliminating the clutter of paper receipts.

Break free from paper clutter ✨

Use Shoeboxed’s Magic Envelope to ship off your receipts and get them back as scanned data in a private, secure cloud-based account. 📁 Try free for 30 days!

Get Started Today2. Categorizes expenses to avoid overspending

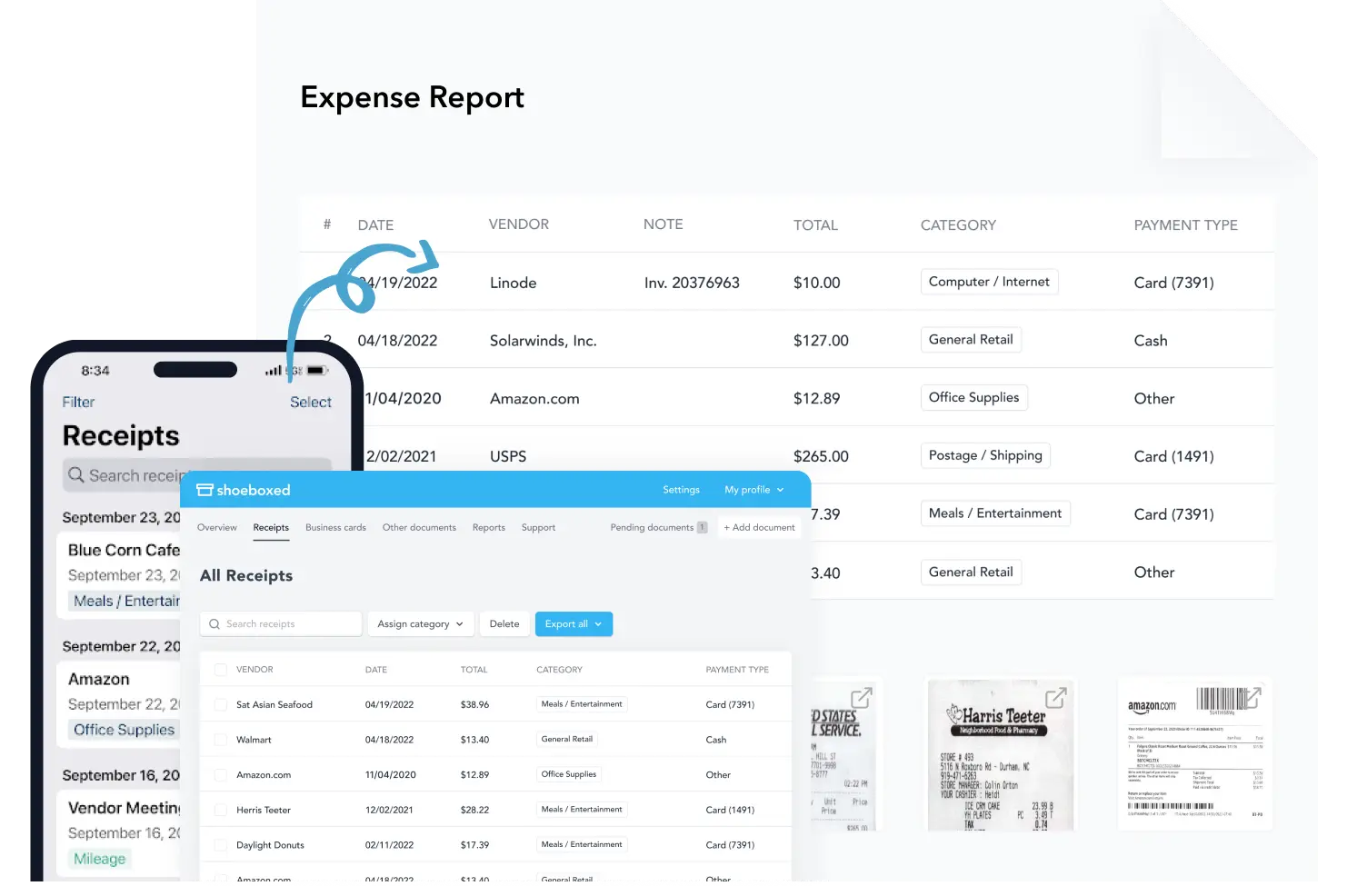

Shoeboxed extracts date, vendor, and amount using OCR (Optical Character Recognition), so you don’t have to enter data manually and automatically categorize your expenses into tax or expense categories.

Create custom categories to fit your own business needs. This will help you keep accurate records for tax prep or financial analysis.

Shoeboxed organizes your receipts so you can see where your money is going. By spotting your spending habits, you can cut unnecessary expenses and put more money towards paying more than the minimum on your next credit card bill.

3. Budgeting for higher payments

Shoeboxed’s reporting features let users summarize all expenses and transactions for a running total so you can see how much is going where.

With Shoeboxed’s categorized expense reports, you can see your monthly spending and cut back to areas where you can. Those savings can then be applied to your credit card balance, reducing interest and getting you out of debt faster.

4. Tracking spending for credit utilization

High credit card balances can hurt your credit score. Shoeboxed keeps your records in check so you can track your spending and avoid building up balances that will only let you pay the minimum.

5. Payoff goal planning

Use Shoeboxed to track deductible expenses and organize tax documents. If you get a tax refund, Shoeboxed will have all your financial info at your fingertips so you can apply those extra funds to your credit card balance.

Example

You’re on a tight budget but want to pay more than the minimum on your credit card.

With Shoeboxed, you can:

Upload and categorize all your receipts.

Run a report to see where you’re spending discretionary money, like dining out or subscriptions.

Adjust your budget and apply those savings to your credit card balance.

Shoeboxed gives you control over your finances by showing you where your money is going. By using their platform as part of your financial plan, you can make smart decisions, cut out unnecessary spending, and pay more than the minimum each month.

You’ll save interest and get out of debt faster.

Turn receipts into data with Shoeboxed ✨

Try a systematic approach to receipt categories for tax time. Try free for 30 days!

Get Started TodayTips for managing your credit card minimum payment

In addition to using Shoeboxed to keep track of expenses, start by taking a look at your household budget and finding ways to cut back on your spending.

Consider canceling a few streaming services or cutting back on takeout meals to set aside enough money for your credit card minimum payments.

If you’re still short, you can always ask your credit card issuer to reduce your minimum payment.

Paying at least the minimum due on time each month is crucial to avoid penalties and interest charges.

If you’re struggling to make payments, reach out to your card issuer to inquire about relief options that may be available.

Strategies for reducing credit card debt

I have found some effective strategies that will help reduce your credit card debt.

Debt pay-off methods like the Snowball and Avalanche methods can help.

Making multiple payments or taking on a side hustle can also help pay off credit cards faster.

Consider using a debt pay-down method or Bright Money to avoid interest costs and pay off your credit card debt faster.

Also, look into 0% balance transfer credit cards to help you save on interest and pay off debt faster.

Setting up automatic payments

Setting up automatic payments can help ensure a cardholder doesn’t miss a payment due date.

The process for setting up these payments varies depending on the credit card's terms and issuer.

Automatic payments can help you avoid paying late fees and penalty APRs.

You can set up automatic payments through your credit card issuer’s website or mobile app.

Frequently asked questions

Can I pay more than the minimum?

Yes, you can always pay more than the minimum, and you should reduce your interest rate and pay off debt faster.

What if I only pay the minimum for a long time?

Paying only the minimum will result in higher interest charges, longer debt repayment, and potentially lower credit scores due to higher credit utilization.

In conclusion

The minimum payment keeps you in good standing with your credit card company but it shouldn’t be a long-term strategy.

What’s a reason to pay more than the minimum on your credit statement each month?

You should pay more than the minimum on your credit card to save interest, pay off debt faster, and improve your credit score. By paying more and managing your finances effectively, you can avoid the pitfalls of debt and build a better future.

Caryl Ramsey has years of experience assisting in different aspects of bookkeeping, taxes, and customer service. She uses a variety of accounting software for setting up client information, reconciling accounts, coding expenses, running financial reports, and preparing tax returns. She is also experienced in setting up corporations with the State Corporation Commission and the IRS and is a contributing writer to SUCCESS magazine.

About Shoeboxed!

Shoeboxed is a receipt scanning service with receipt management software that supports multiple methods for receipt capture: send, scan, upload, forward, and more!

You can stuff your receipts into one of our Magic Envelopes (prepaid postage within the US). Use our receipt tracker + receipt scanner app (iPhone, iPad and Android) to snap a picture while on the go. Auto-import receipts from Gmail. Or forward a receipt to your designated Shoeboxed email address.

Turn your receipts into data and deductibles with our expense reports that include IRS-accepted receipt images.

Join over 1 million businesses scanning & organizing receipts, creating expense reports and more—with Shoeboxed.

Try Shoeboxed today!